EDA is an essential design tool software for the IC electronics industry and is a prerequisite for the realization of ultra-large-scale integrated circuit design. At present, the EDA industry is highly monopolized by the three giants from abroad, and there is also a huge gap between domestic EDA and Big Three technologies. The recent discussion of domestically produced chips from a technical point of view is full of enthusiasm. The author of this article has taken the initiative to propose a “cost-equity conversion investment†model, which attempts to explore the path of the rise of domestic EDA from a business model innovation. It is refreshing.

The author, like watching the sunrise, snow without traces, and Seidang, also graduated from the microprocessor research and development center of Peking University (MPRC is this to be the rhythm of the red nets). The ZTE event set off intense attention and heated discussion from the government to the people. Even the middlemen who sell the house chatted with me about ZTE and talked about chips. Even the children in my kindergarten came back and told me that ZTE was bullied by American robbers because he Daddy with classmates worked in ZTE.

This is also a very good patriotic education. People suddenly discovered that the original song and dance have been flat and their years have been quiet. However, others have not yet pulled the trigger.

The author has been engaged in the chip design industry for more than ten years, and took his familiar EDA as an example, taking Xiong Wen of Seidong's younger brother as "a breaking point of the Chinese core" as a big proposition. He talked about the rise of the business model innovation of domestic EDA and hoped to integrate it with socialism. Circuit business is adding bricks and tiles.

The status of EDA

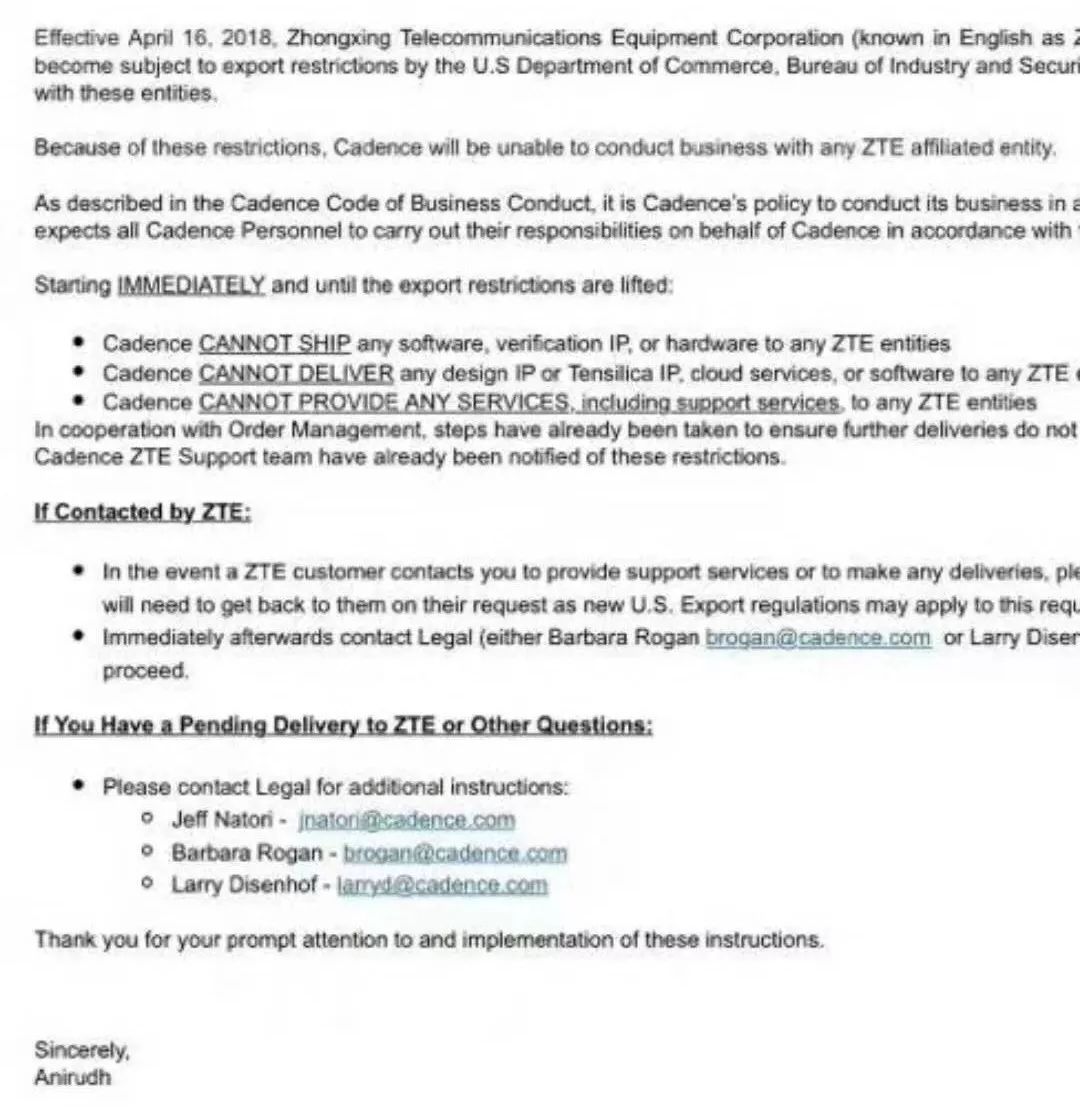

In the US sanctions against ZTE, in addition to prohibiting the sale of chips to ZTE, the most basic EDA tool is naturally a major killer in the United States. Recently, the world's largest electronic design automation (EDA) company Cadence's internal mail outflow, the e-mail said it will stop the ZTE service.

(Photos from the Internet)

What is an EDA tool?

EDA tool is the abbreviation of Electronic Design Automation. It is developed from the concepts of Computer Aided Design (CAD), Computer Aided Manufacturing (CAM), Computer Aided Testing (CAT) and Computer Aided Engineering (CAE). Using EDA tools, the engineer will complete the process of circuit design, performance analysis, and design of the IC layout by the computer.

EDA is an essential design tool software for the IC electronics industry and is the most upstream sub-industry of the IC industry chain. Prior to the absence of EDA tools, the circuit must be hand-crafted. It is simply not possible to design a large-scale integrated circuit with hundreds of millions of transistors. It can be said that with the EDA tool, there is the possibility of VLSI design.

What is the current status of the global EDA industry?

After a constant market reshuffle, the EDA industry has been reduced from the turbulent times in the 1980s to the current global giants Cadence, Synopsys, and Mentor Graphics, becoming a highly monopolized industry.

Of course, there are EDA companies in China, but some analysts have pointed out that the technology gap between China's domestic EDA companies and foreign EDA giants is at least 20 years. In particular, Cadence, Synopsys, and Mentor have consistently ranked in the top three of the EDA industry. 70% of the industry's total revenue is loaded into their pockets.

What is the business model of the EDA industry?

EDA companies use the EDA tool license fee as their main business model. Take the example of a PDN tool of an EDA company. The license fee for a three-year license is about 1 million US dollars. For chip design companies, generally need to purchase multiple sets of licenses to meet the chip design requirements.

The rise of domestic EDA business model innovation

Since there is a huge gap between domestic EDA and the technology of the three giants abroad, and according to the current business model, there is almost no ability for positive competition. Can we change the gameplay?

Let us first take a look at the drawbacks of the business models of the three major foreign EDA giants. Due to the high price of license, generally only large players can afford it. Taking MediaTek and Huawei as examples, in 2010, MediaTek and Cadence signed an order for 50 million dollars. At the end of 2014, Huawei and Cadence signed an order of 30 million dollars. For start-up companies and small companies, it is difficult to pay EDA's high license fees under the pressure of design costs and manufacturing costs and the long design cycle. (The issue of piracy licenses is not discussed here. After all, over the past decade or two, the development has proven that piracy can't save the country. With the country’s emphasis on intellectual property rights, copyright protection has become more and more stringent, given that China has such a huge amount. Science and engineering talents, intellectual property rights are also and will become China's advantages)

For domestically produced EDA, since we cannot implement positive PK, we may be able to adopt a new business model, tentatively calling it the “cost-equity conversion investment†model (the name may not be professional enough, forgive me for not being like Lin Fufu like Seidong’s brother. The teacher's lesson), which does not rely on the sale of licenses as the main income, but instead uses the license to compose the shares of start-up companies or small and medium-sized companies to cultivate their own soil for survival. After the companies become bigger and stronger, they are listed for high equity returns.

This business model has the following advantages:

Reduced the chip design company's entrepreneurial threshold. The 19th CPC National Congress has clearly placed the integrated circuit industry in the first place in the real economy. After the ZTE incident, the IC industry will be upgraded to a higher strategic position. With the central and local support policies for the IC industry With the introduction, there will also be a large number of IC start-up companies. This business model will further encourage the emergence of start-up chip design companies and cultivate their own soil.

Deep binding with the company in which shares were invested. Only by investing in a company that grows and grows, can a successful listing be used to obtain returns. It is inevitable that it will be tilted in terms of resources and in-depth cooperation with the service, so as to increase the success rate of the company.

The return on equity returns will be higher. For example, if you want to buy a genuine license in order to start a business, then you may have 100 small companies willing, because the high initial investment, only 20 small companies start a business, if each startup company to pay 1 million US dollars a year license fee In terms of five years, the total income is 100 million US dollars. If the business model of licenses is used as a shareholder, because the early-stage investment threshold is reduced, these 100 willing small companies will start their own businesses. Assume that each company has a share of 10%, and if there are 20 companies listed on the market after five years, The average market value of 1 billion US dollars is calculated, the equity value of 2 billion US dollars. Of course, the data is not accurate, just to illustrate that this model may be another kind of business model that can be bigger and stronger for domestic EDA manufacturers.

Guarantee continuous income. Because of the equity investment, after the shares are listed, they can also sell licenses to ensure continuous income.

If this business model is called a strategy, what is the feasibility of this strategy? Let us turn our attention to several classic battles in the three industries of chip, Internet, and communications.

ARM VS Intel: Before 2003, Intel seemed to be invincible, not only occupying most of the market share of x86 architecture CPU in the desktop area, but also taking over almost all RISC architecture CPUs and occupying servers. market. His business model is to sell his own research and development of general-purpose CPU, with the windows operating system, constitute the most core components of desktop computers. However, with the rise of mobile phones in early 2000, especially the rise of smart phones and mobile Internet, ARM has gradually become the dominant player in the mobile field, occupying most of the market share of the low-power CPU market, and putting Intel’s x86 architecture CPU Atom defeated. His business model is not to sell CPU, only authorized IP and architecture, which has attracted Qualcomm, MediaTek, Apple, Samsung and other companies based on his architecture to develop low-power CPU, built a huge ecosystem. Please refer to another Xiongwen article "From the Intel and ARM competition, see how difficult it is to make a chip."

Taobao VS ebay eBay: ebay was founded in 1995 and acquired eBay in 2003. Taobao was established in 2003. When eBay was founded, eBay has become the myth of Silicon Valley in the United States. In 2003, the transaction volume was 23.8 billion U.S. dollars and the net income was 2.2 billion U.S. dollars. The total turnover of Taobao was only 34 million RMB. This was a war that appeared to be seriously unequal at the time. But in 2005, Taobao surpassed eBay eBay and began to put competitors far behind. In May, Taobao surpassed Yahoo Japan and became the largest online shopping platform in Asia. In 2005, the turnover exceeded 8 billion yuan, surpassing Wal-Mart. In 2006, Taobao became the largest shopping site in Asia. In 2009, it has become China's largest integrated store, with annual turnover of 208.3 billion yuan. Also as an e-shopping platform, eBay eBay has adopted a fee-based business model, and Taobao has attracted numerous Taobao shopkeepers thanks to its free business model, which has won the war and made itself a success.

Huawei VS Ericsson: In the late 1980s and early 1990s, China’s communications market was basically divided by European and American giants. When Huawei was founded in 1987, Ericsson had a history of more than 100 years and owned 40% of the 2G/GSM area. Market share and nearly 50% market share of 2.5G/GPRS has become the undisputed leader in the communications industry. Faced with the monopolistic advantages of European and American giants, Huawei adopted a model of encircling the cities from rural areas. By 1995, sales had reached 1.5 billion yuan, mainly from the Chinese rural market, but it had established a firm footing. In 2013, Huawei was the first to surpass Ericsson, the world’s largest telecommunications equipment supplier, and maintained it to this day.

From the classic battles of these three industries, we can see:

When technology and market are at a disadvantage, you may want to consider business model innovation, change gameplay, and not compete with your opponent. The "cost-equity conversion investment" model has changed the gameplay of EDA giants and avoided positive competition with them.

Cultivate the soil that oneself survives, namely the ecological circle, make oneself succeed while helping the customer succeed too. The “cost-equity conversion investment†model has reduced the investment threshold for chip design companies and cultivated their own soil. It is deeply tied up with customers, and when customers are successfully listed, they have also received substantial equity returns. To build an ecosystem in this mode is somewhat similar to the Internet gameplay method. It first acquires users, and when the user base is large, traffic is realized (company listing, return on equity). Therefore, it is not a joke to look at Sunrise's Xiong Wen's "China's Core Setbacks, Never Stops," and the fact that chips are used to save the country and rely on BAT is probably not a joke. Perhaps it should include drawing BAT games into the chip industry.

The strategy of encircling the cities in the countryside is not only suitable for military warfare but also for commercial warfare. The “cost-equity conversion investment†model aims to target the small and medium-sized companies (similar to rural areas) that the EDA giants do not see, which are relatively small and risky. This is a hard nut to crack, but there is hope. Allowing you to survive and grow, while narrowing the technological gap, may even surpass it as Huawei.

When it comes to allowing domestic EDA manufacturers to survive and grow, while narrowing the technological gap, we might as well prove it technically.

Although the EDA industry is part of the integrated circuit industry, it does not follow Moore's Law like a process, but has its own special development rules, because the algorithm cannot be upgraded every 18 months.

Taking Synopsy's PnR tool as an example, Astro can be basically used before 130nm, ICC is introduced from 90nm to 28nm, and ICC2 is introduced after 16nm. Each generation of tools can use almost 3-4 process nodes, ie, 5-7 years, with relative stability. And EDA tools have developed to today, the algorithm is relatively mature, and there are few disruptive innovations. The relatively stable time window and the maturity of the algorithm have given more possibilities to narrow the technological gap than other aspects of the integrated circuit.

The above discussion is about the strategic feasibility of the "cost-equity conversion investment" model. If the strategy is feasible, it can be tactically decomposed. Since the country is fully committed to the development of the integrated circuit industry, EDA is also an indispensable part. Considering the cash flow pressures of the earlier stage of the model, it can be supported by the state in advance, and the tactics can be divided into two steps.

In the first step, the national mandatory current chip design companies must use domestic EDA on some low-end products, expand the use of domestic EDA, enhance the domestic EDA's technical level, and form a positive feedback to reduce the domestic EDA and foreign countries. The level of technology may consider giving certain tax incentives or other incentives.

In the second step, domestically produced EDA can be implemented in a cost-equity conversion investment business model after the above companies have matured in terms of reliability and practicability. This model is adopted by a large number of companies emerging from the national integrated circuit strategy development. And in-depth cooperation, develop their own ecology, establish a moat, improve the success rate of small and medium-sized companies, and form a positive feedback, eventually achieving the curve overtaking.

For the first step, a brother who has moved from chip design to investment has also made a good suggestion after he has read this model: “This EDA VC model is a little too advanced, and it challenges the EDA company's cash flow. But it can be There is a compromise, the securitization of receivables assets, let the financial market to solve, so that investors with high risk preferences to buy. "

Using the "cost-equity conversion investment" model, a model for incubating Design House from EDA can finally be formed. Actually, the same has been used as the foundry of integrated circuit infrastructure platform. There have been successful cases: UMC has passed through the incubation of MediaTek, the United Kingdom, etc. By contacting Design House, on the one hand, you can guarantee your own production capacity, and on the other hand you get a generous return on equity.

The "cost-equity conversion investment" model is more feasible for EDA as a software service provider. In addition, this model may also be adopted for IP vendors. Moreover, the "cost-equity conversion investment" model should not only be limited to EDA or IP but also be adopted in many industries. The test is the player's strategic vision and execution.

From the end of Ps to the end of the text, a senior brother told me that domestically produced EDA has indeed been catching up technically and has even achieved a temporary lead in some local areas. For example, domestic EDA manufacturers Huada nine-day products ICE hard rely on their own strength, rather than the national mandatory, sold to a lot of big factories. In addition, Hangzhou Guangli has done a good job in the foundry yield test analysis tool.

Dong Senhua, the product director of Huada Jiutian, began researching and developing domestic EDA when I was still in the laboratory. At the moment when many domestic cattle have given up on their dreams due to reality, he focused on domestic EDA for fifteen years, making people feel moving and worthy of admiration. No matter what, we should call them for Call!

360 Laptop

360 laptop sometimes is also called as Yoga Laptop , cause usually has touch screen features. Therefore you can see other names at market, like 360 flip laptop, 360 Touch Screen Laptop,360 degree rotating laptop, etc. What `s the 360 laptop price? Comparing with intel yoga laptop. Usually price is similar, but could be much cheaper if clients can accept tablet 2 In 1 Laptop with keyboard. Except yoga type, the most competitive model for Hope project or business project is that 14 inch celeron n4020 4GB 64GB Student Laptop or 15.6 inch intel celeron business laptop or Gaming Laptop . There fore, just share the basic parameters, like size, processor, memory, storage, battery, application scenarios, SSD or SSD plus HDD, two enter buttons or one is also ok, if special requirements, oem service, etc. Then can provide the most suitable solution in 1 to 2 working days. Will try our best to support you.

To make client start business more easier and extend marker much quickly, issue that only 100pcs can mark client`s logo on laptop, Mini PC , All In One PC, etc. Also can deal by insurance order to first cooperation.

360 Laptop,360 Laptop Price,360 Flip Laptop,360 Touch Screen Laptop,360 Degree Rotating Laptop

Henan Shuyi Electronics Co., Ltd. , https://www.shuyicustomlaptop.com